Changing the structure of local government revenue generation

The Wall Street Journal has been running a series of articles on city finances, and the latest article, "Cuts in State Aid Leave Cities Reeling," focuses on the impact of cuts in state aid to cities, using Providence, Rhode Island as an example.

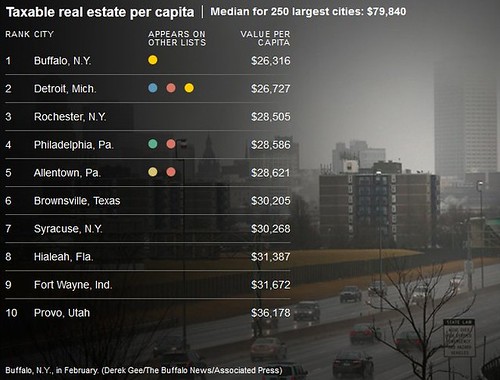

A WSJ interactive feature on the economic status of the largest cities in the US provides comparative data on population, number of days of cash on hand, financial reserves, taxable real estate per capita, net direct debt per capita, pension costs and state aid.

Not quite 17% of Providence's budget came from state aid in 2007, and last year it was about half of that figure. This is one of the highest percentage drops experienced amongst the nation's 250 largest cities, and has been devastating to the city's budget.

In response the city has cut expenses, raised residential and commercial property taxes, especially commercial property taxes, imposed a personal property tax on motor vehicles, and has been much more aggressive in pushing the city's nonprofits--which hold 39% of the city's land--to provide "Payments in Lieu of Taxes." The nonprofits have been resistant, but are coughing up some money.

What is the best way forward to "solve" the financial problem of hard pressed cities and towns?

Obviously, financing local government is a problem for most cities as the result of a quintuple whammy of outmigration of residents and businesses; deindustrialization; the recession, which battered tax revenues; and poor financial decisionmaking in the past (such as unfunded pension liabilities or a variety of bond-funded initiatives that were poorly executed, such as in Harrisburg, PA or in Jefferson County, AL).

Losing state and/or federal funds pushes local governments, but particularly cities, to the brink. How local governments are funded needs to change.

Changing the framework

In "Detroit and the New York Times" I wrote that there are four primary approaches that react to material changes in financial and economic conditions faced by local governments, by reorganizing the structure and scale of local government and how it is financed. But really there are three approaches:

- one has to do with the scale of government, adding to the volume of taxable properties as a taxation method by combining jurisdictions;

- the second has to do with the organization of government, and merging services across jurisdictions, while not necessarily merging over-arching governmental bodies;

- the third has to do with taxation and what is allowed to be taxed.

- merging of the center city and the county (e.g., Indianapolis, Nashville, Lexington, Louisville, New York City in 1898, Toronto, Montreal, etc.)

- not merging the center city and county but having strong metropolitan scale planning and governance institutions, especially for transit (Minneapolis; Portland, Oregon)

- tax revenue sharing across a metropolitan area (Minneapolis)

- special tax-service districts that operate across a city-county-region (Regional Asset District, Allegheny County, PA; Huron-Clinton Metropolitan Parks Authority, Southeastern Michigan).

These three writer-academics are probably the biggest proponents of the harmonization of taxing, funding, and certain elements of planning and governance on the metropolitan scale:

-- Gerald Frug, Harvard University

-- Myron Orfield, Institute for Metropolitan Opportunity, University of Minnesota Law School

-- David Rusk, Inside Game/Outside Game: Winning Strategies for Urban America

Government mergers at a smaller scale

Another element that I didn't include in the March list is a fifth, various mergers of government-provided services across jurisdictions, at a level smaller than center city and county, such as library systems, small police departments getting absorbed by county police departments, mergers of smaller special services districts into larger, more consolidated districts, etc. Most recently this has been pushed by Gov. Christie in New Jersey ("NJ voters support merging school districts, local governments," from the Newark Star-Ledger and "Princeton Merger Vote Tests Christie's Attempt to Shrink Towns" from Bloomberg ) and is happening in the Midwest especially between hard pressed local governments for the last 10 years or so, but it isn't a phenomenon limited to the Midwest (e.g., "Santa Ana disbands Fire Department in bid to rescue budget" from the Los Angeles Times, or this blog entry "Cook County and City of Chicago partner on certain operations: Save $20 million").

De-annexation

A variant of merger is annexation, which is a long time phenomenon. Usually annexation of unincorporated township or county land by an adjoining city occurs in order to increase tax base, provide access to "city water" and other services, etc. But now some communities are doing de-annexation, giving up land to another jurisdiction, to cut costs. See the blog entry "Annexation as a strategy for saving counties money: Cook County, Illinois."

Tax base sharing

According to a paper by the New York State Commission on Local Government Efficiency and Competitiveness:

In a tax-base sharing approach, each municipality shares in the increase in property value that occurs in a specific area after a certain date. Tax-base sharing is intended to:But sharing tax revenues across jurisdictions occurs only in two places in the United States, Greater Minneapolis and the Meadowlands area of New Jersey. And in metropolitan regions that cross state boundaries such as Philadelphia, Washington, DC, Chicago, Wilmington, and New York City, it would be impossible.

• Reduce competition among communities for commercial and industrial properties to add to their tax bases.

• Create a fairer distribution of tax benefits from properties that impact on and are supported by surrounding communities.

• Reduce disparities in tax bases.

• Promote orderly urban development, regional planning, and smart growth by reducing the impact of fiscal considerations on the location of business and residential growth; of highways, transit facilities, and airports.

So while I am intellectually attracted to this approach, and in our area we see the necessity of it in Virginia especially as cities and counties are legally separate, and therefore there isn't the opportunity to share sales taxes across jurisdictions, something that can happen with a more typical county organization of the taxation process at the sub-state level, the likelihood of pulling this off in most places is nil.

Other approaches are needed.

(Note that the federal government did do revenue sharing from 1972-1986. See the 1980 GAO report, Changes in Revenue Sharing Formula Would Eliminate Payment Inequities; Improve Targeting Among Local Governments and "END OF FEDERAL REVENUE SHARING CREATING FINANCIAL CRISES IN MANY CITIES," New York Times.)

Local income taxes

Most cities are reliant on property and sales taxes for the bulk of their revenues. The vagaries of these sources--lack of stability and their declining nature, except in the most economically robust communities--ought to push states to reconsider how local government funding occurs.

Some cities, usually the largest in the country, like New York City, have imposed income taxes for a long time. The primary purpose is to tax income earned in the city by nonresidents. But most cities do not have income taxes or are not able to levy such taxes based on state law.

In March I wrote about this, "Economic restructuring of cities: Detroit etc. (with a comment on local income taxes)," suggesting that states should include a local income tax as part of the state income tax filing process.

Local income taxes are controversial, and business organizations usually are against such taxes, and jurisdictions that don't impose such taxes recruit and market against the cities that do. If "everybody does it" a level playing field is created.

In that blog entry, I mention how Maryland has a local income tax, but it is collected by the State as part of the annual income tax filing process. The rate does vary by jurisdiction. It doesn't insulate local jurisdictions from having to be careful stewards of the public monies, but it does help to stabilize funding of local government.

The Maryland method works pretty well as a model.

(Back when Chrysler Corporation was based in the City of Highland Park, Michigan, a local income tax assessed mostly on professional workers at Chrysler generated the bulk of the city's revenue, along with commercial property taxes on the Corporation's property. When Chrysler moved to the suburbs--Highland Park is a community surrounded by the City of Detroit--Highland Park became destitute. See the past blog entry "Urban decay and sprawl: one community's gain at the expense of another's.")

Service payments instead of property taxes from nonprofits

While I think it's reasonable to give nonprofits a tax exemption, I think it's also reasonable for nonprofits to pay for the services portion of what property taxes normally cover. For example, for emergency services, schools (in Ann Arbor, Michigan, University of Michigan student families may send their children to the local schools, but the school district gets no money from the University to defray the cost), infrastructure provision, etc.

That's the point of PILOTs, to collect some tax equivalent money from nonprofits to help cover the cost of government/provision of public services. This is especially important to cities, where as much as 50% of the land in some places may be tax exempt.

When I was a child, I seem to recall that the federal government recognized this impact on local jurisdictions and did provide some monies to jurisdictions based on the presence of federal installations in their communities. This was separate from the federal revenue sharing program.

-- Payments in Lieu of Taxes: Balancing Municipal and Nonprofit Interests, Lincoln Land Institute

-- Taxes, Fees, and PILOTs, National Council of Nonprofits

-- PILOTS Taking Off, University Business Magazine

Separately, Providence proposed that nonprofit entities with more than $20 million in property should have to pay the equivalent of 1/4 of the property tax that would be assessed on commercial property. This was at the height of the current recession. See "City wants new tax on colleges, hospitals" from Providence Business News.

Taxing unrelated business income/possessory interests

Although there is another issue for which I don't know the details, such as whether or not nonprofit property that is used for unrelated revenue generating purposes is also taxed. For federal tax purposes this is covered by a tax on unrelated business income.

This is an issue in DC for example, because George Washington University owns a great deal of property that is commercial used for functions not related to the university. Typically, a food operation that mostly serves students and faculty would be exempt from tax. But what about a building leased to an unrelated organization like the World Bank or the local utility company?

In DC in terms of federally owned property used for profitmaking purposes, such as Union Station, the city assesses property tax payment equivalents. This type of property tax is called a "possessory interest tax."

Union Station challenged this for awhile, but has since capitulated (see "D.C., Union Station Redevelopment Corp. settle tax dispute," from the Washington Business Journal).

Note also that when government agencies lease space in privately owned buildings, the property owner ends up paying property and income taxes as a result, whereas this wouldn't happen if the agency were located in an agency-owned building.

Fees assessed on students enrolled in local universities and colleges

Another way to raise money from nonprofit institutions of higher education is to somehow impose a fee on each student that is paid to the locality.

Pittsburgh proposed a tax on student tuition ("Pittsburgh Pushes Tax on College Students," Wall Street Journal, "Pittsburgh's mayor drops tuition tax," Pittsburgh Post-Gazette) and Providence proposed a fee per student ("Mayor Proposes a College Attendance Head Tax In Rhode Island," Tax Foundation; "Student Fee Would Break Bond of Trust," an op-ed by the President of Providence College).

The Providence proposal was criticized in part because it was aimed at private institutions only, although this was a convenience, because local governments can't impose taxes on higher governmental authorities (state or federal) without their consent.

Neither proposal was approved, but in both instances pressure was created on the colleges to make PILOT payments.

Conclusion

I would recommend three policy changes at the state level and one at the federal level, to assist local governments in attaining funding stability and economic sustainability through taxation practices. (Mergers are a different issue and should be pursued as well.)

First would be for states to set up a local income tax percentage as part of the state income tax collection system such as how Maryland does it. (I don't know what to recommend for those states, like Alaska or Washington or Florida without a state income tax.)

Second would be to set a state policy that structures the imposition of PILOTs, rather than expecting each locality to figure it out on its own. That way cities don't have to try to do student capitation taxes either.

Third would be to clarify taxation policies on property owned by nonprofits but generating income unrelated to their primary function. Procedures should be put into place at the state level enabling localities to assess "possessory interest" and/or "unrelated business" taxes. And the legality of this practice with regard to federal property should also be clarified by the federal government as well.

Fourth would be a PILOT equivalent for federal lands and installations. I remember there being such a program in the 1960s, but I could be wrong. It bears further research. I might just be thinking of the federal formula for revenue sharing.

Such payments could help to reduce rural resistance to federal land ownership, a problem that is particularly pronounced out west, where a great deal of property is federally owned, especially in Utah. See this op-ed, "Black Diamond CEO: Shutdown exposed folly of Utah's federal-land grabbers," from the Salt Lake Tribune.

And in those situations where the federal land portfolio doesn't really need a particular property (see the book Who Is Minding the Federal Estate?: Political Management of America's Public Lands, "GSA completes sale of West Heating Plant for $19.5 million" and "GSA to auction off Bethesda building" from the Washington Business Journal) maybe having to make such payments would include faster right-sizing of the federal land portfolio as another benefit.

Labels: annexation, City-County mergers, electoral politics and influence, government organization, property tax assessment methodologies, provision of public services, public finance and spending

posted by Richard Layman @ 12:13 PM&Permanent Link

![]()

![]()

{kind=link}

{kind=link}

3 Comments:

I think the larger problem is the market for tax free muni bonds in the US is tapping itself out.

Felix Salmon had a good summary of sovereign debt and the difference between liquidity and solvency.

http://blogs.reuters.com/felix-salmon/2013/11/02/chart-of-the-day-sovereign-precariousness-edition/

Another way to read this is smaller governmental entities are being priced out. The US can't default on their debts -- Obama's statement aside you just print more money. DC, or NY, or Puerto Rico aren't in those situations.

So what we are having is a wealth transfer from poor places to richer ones, rather than the other way around.

At some point we are probably going to have to federalize city pensions to spread the costs around.

I'll check out that article. Of course, one of the reasons I favor a height increase is it would allow us to increase our municipal debt (although I only want to use it on "good things").

Thank you for providing such a valuable information and thanks for sharing this matter. to get Online pharmacy from online medicine store.

Post a Comment

<< Home